By Alexander Melikishvili

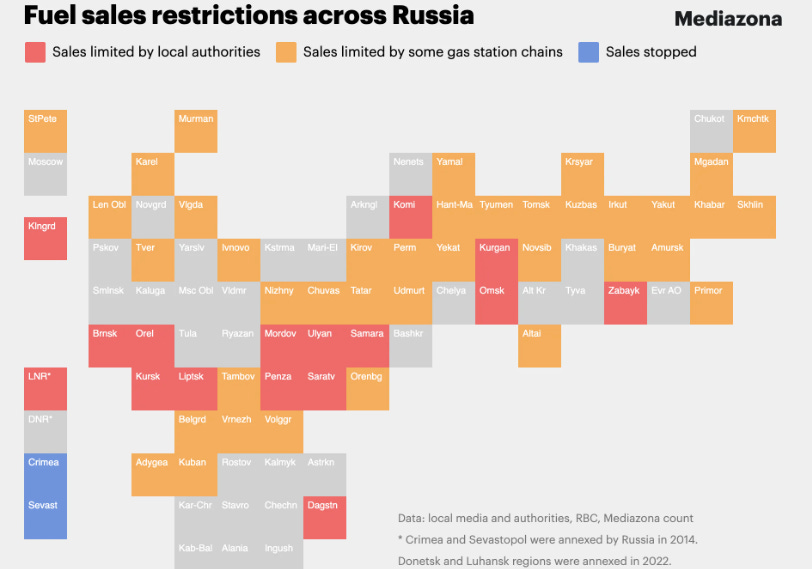

Ukraine’s “kinetic sanctions” (drone and missile strikes targeting Russia’s oil and gas sector, including oil refineries) finally forced the Kremlin to acknowledge that these relentless attacks are causing gasoline shortages at a time when domestic demand is peaking due to the summer vacation season. On June 28, President Putin for the first time publicly admitted that the Ukrainian attacks have resulted in “a certain shortage,” but called it “not critical.” In fact, the Russian leader is grossly understating the scale of the problem. According to the Russian investigative platform Mediazona, as of June 26th, some form of fuel rationing was in place in 56 out of 83* regions comprising the Russian Federation. Furthermore, brawls often break out in long lines at gas stations, undermining social stability to the extent that this has already prompted local authorities in at least one location (the Black Sea resort town of Anapa in Krasnodar Territory) to employ Cossack volunteers to maintain public order at the pumps.

*Russian fuel restrictions by region: Image source: Mediazona

In June alone, the Ukrainian military struck eleven refineries across Russia, according to Ukraine’s defense ministry. By early July, the Ukrainian General Staff was reporting that Ukraine had knocked out 42% of Russia’s refining, costing Moscow $13.5 billion in losses since August 2025. Earlier, the Associated Press had reported, quoting the Macro-Advisory consultancy, that these attacks had caused the destruction of about one-third of Russia’s refining capacity, a major milestone for Ukraine. Even Russian government statistics, which should be treated with extreme caution as they are most likely manipulated to create a more favorable picture, indicate that gasoline production has been reduced by 17% to 850,000 barrels a day.

In response to the escalating crisis, on June 1, the Russian government introduced the first-ever ban on the export of jet fuel, which is to remain in effect until November 30. This comes after a restriction on the export of petroleum that has been in place since April and is due to expire at the end of July. Russia’s Deputy Prime Minister Alexander Novak also revealed that the authorities are considering a ban on the export of diesel fuel. The situation must be really dire if Russia, one of the world’s top energy exporters, is resorting to such measures.

A Friend in Need: Russia Turns to Belarus and Kazakhstan

To remedy the situation, Russia plans to import 400,000 tons of gasoline per month, according to an anonymous industry source, as reported by Reuters on July 1. However, considering that Russia’s daily consumption of petroleum in summer reaches 110,000 tons, this volume will not be sufficient. Moreover, as Alexander Kolyandr at the Center for European Policy Analysis (CEPA) points out, Ukrainian drone strikes have affected eight out of the ten largest refineries in Russia that currently produce about 85,000 tons of gasoline daily, leaving a shortfall of 25,000 tons per day. Consequently, Russia leaned on its long-time ally Belarus, leading to a threefold increase in Belarusian petroleum exports delivered to Russia by rail in the first half of June compared to May, reaching more than 70,000 tons. Belarus is opportunistically profiting handsomely from this arrangement as it has hiked the price of gasoline it sells to Russia. Since May, it has almost doubled to $1,646 per ton, as the Russian business daily Kommersant reports. However, given Russia’s daily consumption, Belarusian petroleum exports are simply not enough.

While Russia has turned to Kazakhstan for help, the degree of influence it wields over Astana is significantly different, which explains why the assistance it has been promised is less significant. Industry sources in Kazakhstan told Reuters that Kazakhstan agreed to supply 50,000 tons of gasoline (Ai-92 and Ai-95) to Russia in July and August as humanitarian assistance. They also noted that the Kazakh side was not enthusiastic about this because it would strain the already tight gasoline market in Kazakhstan while raising potential sanctions risks. It should be noted that, as of July 2, the Kazakh government officially denied receiving any requests for petroleum from Russia, according to Kazakhstan’s Minister of Energy Yerlan Akkenzhenov. Regardless of the veracity of the report by Reuters, which is likely credible, Kazakhstan is dogged by limited refining capacity.

To avoid shortages on the domestic market, Kazakh authorities banned the export of gasoline, diesel fuel, and other oil products, starting from November 2025. Since then, this ban has been extended twice, most recently in April, and it is due to expire in November. However, on 3 July, the energy ministry published a draft law that will extend the ban from November to May 2027.

Outlook

Given production and refining constraints in Kazakhstan and Belarus, they are unlikely to mitigate Russia’s deepening fuel crisis. Nonetheless, this presents Kazakhstan with a excellent opportunity to demonstrate its symbolic loyalty to Russia, even as it balances that relationship against its growing ties with the EU and the United States.

On both fronts, Kazakhstan can boast significant achievements, especially with regard to the European Union, as demonstrated by President Tokayev’s visit to Brussels in June that was preceded by the conclusion of $462 million worth of agreements to deepen connectivity between Kazakhstan and the EU via the Middle Corridor.

Kazakhstan’s constraints are systemic due to its considerably underdeveloped refining capacity. With only three main refineries (located in Pavlodar, Atyrau, and Shymkent), Kazakhstan’s aggregate refining capacity is only 18 million tons annually even though the country produces about 100 million tons of oil per year. The government unveiled ambitious plans for boosting refining capacity, but even the recently accelerated timeline envisions increasing it to 40 million tons only by 2033. This provides Tokayev with the perfect excuse to decline further requests from Russia without angering either the Kremlin or Ukraine.

Unable to shore up support in the “near abroad,” Russia is turning its attention further afield. Naturally, India, as the second-largest buyer of Russian crude in the world in May, emerges as the most reliable option. Reuters reported on 1 July that a shipment of 60,000 tons of gasoline was en route from India to Russia by sea, loaded on two tankers. The Indian energy minister Puri’s superficial denials notwithstanding, anonymous sources with direct knowledge of the relevant deals told Reuters that the said shipment originated with the Indian refiner Nayara Energy, which is 40%-owned by Rosneft. India gets Russian crude at a significant discount, but it’s likely that Russia receives gasoline from India at a premium price considering that, as the Indian authorities claim, Russia imports it via intermediaries.

Even if you add all of the above, including Kazakhstan’s likely one-off contribution and supplies from Belarus and India, the combined total falls short of meeting Russia’s summer peak in daily consumption. This, in turn, proves that Ukraine’s strategy of “kinetic sanctions” is effective as Russia is incapable of repairing damaged refineries quickly enough to offset the reduction in refining capacity caused by the Ukrainian strikes. Nor is the Russian government’s ambitious objective of importing 400,000 tons of gasoline per month enough to cover Russia’s daily demand. In addition, Ukraine also has the option of ramping up maritime attacks against tankers delivering gasoline to Russia as well as targeting the key Russian ports where the imported gasoline is unloaded. Apart from substantially increasing public anger in Russia, Ukrainian strikes against refineries also severely endanger Russia’s agricultural sector by derailing the crucial grain harvest season, as farmers complain that they have no fuel to run combines.

*Note: This total does not include Crimea and four other regions of Ukraine (Donetsk, Luhansk, Kherson, and Zaporizhzhia) that Russia unlawfully declared annexed in September 2022.

About the Author:

Alex Melikishvili is a senior country risk analyst with more than a decade of experience working in the private sector (S&P Global, IHS Markit) with a focus on Eurasian security. Alex holds a master’s degree in International Affairs from the George Washington University’s Elliott School of International Affairs.

Thank you for your support! Please remember that The Saratoga Foundation is a non-profit 501(c)(3) organization. Your donations are fully tax-deductible. If you seek to support The Saratoga Foundation, you can make a one-time donation by clicking on the PayPal link below! You can also subscribe to our website to support our work.

https://www.paypal.com/donate/?hosted_button_id=XFCZDX6YVTVKA