Hormuz Blockade Pushes China Toward Continental Energy Suppliers and Overland Routes

The US-led blockade of the Strait of Hormuz has led Beijing to switch to continental suppliers of energy from Russia and Central Asia to offset the disruption of oil supplies from the Persian Gulf.

By Vusal Guliyev

Disruptions to energy flows through the Strait of Hormuz once again reveal the structural vulnerabilities of global oil markets. As the world’s largest crude importer, China is particularly exposed to such shocks. Historically, a significant share of China’s crude oil imports has been sourced from the Middle East, with a substantial portion transiting the Strait of Hormuz.

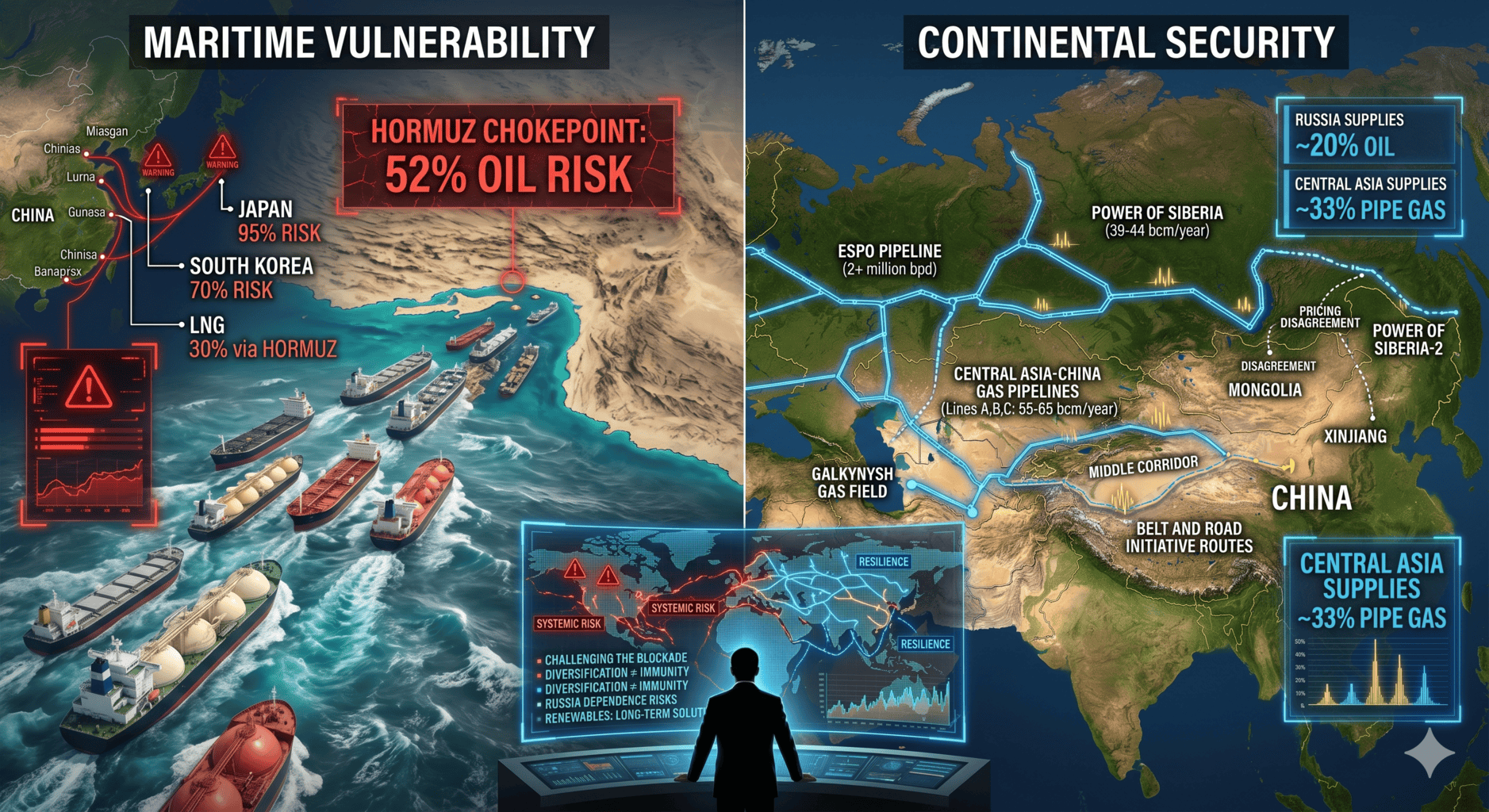

An estimated 52% of China’s oil imports currently pass through the strategic chokepoint. However, Beijing’s dependence remains lower than that of other major East Asian economies. By comparison, around 95% of Japan’s oil imports and roughly 70% of South Korea’s transit the same route. This demonstrates China’s relatively more diversified supply structure than its Asian neighbors. China’s exposure also extends beyond oil. As the world’s largest importer of liquefied natural gas (LNG), about 30% of its LNG imports are linked to flows via the Strait of Hormuz. A considerable share of these supplies originates from Qatar, followed by the United Arab Emirates and Oman.

Against this backdrop, the Hormuz blockade is not merely a disruption but a catalyst, accelerating China’s shift toward continental energy suppliers and overland transport corridors. Over the past two decades, Beijing has pursued a systematic diversification strategy aimed at reducing its reliance on vulnerable maritime routes. As a result, non-Gulf suppliers—particularly Russia and Central Asia—have gained increasing prominence. The current crisis has accelerated this shift. It has reinforced China’s turn toward geographically resilient, land-based energy networks and a broader portfolio of alternative suppliers.

Russia Becomes Beijing’s Fall-Back Supplier

Amid disruptions to Iranian oil exports, Russia has diplomatically positioned itself as a critical fallback supplier for China’s energy needs. During a meeting with Xi Jinping in Beijing on April 15, 2026, Russian Foreign Minister Sergey Lavrov stated that Moscow is capable of fully compensating for any energy shortfall China may face due to the restricted supply of Iranian energy. Unlike Middle Eastern oil flows, Russian exports—particularly via pipelines—remain largely insulated from geopolitical chokepoints and naval disruptions.

Russian crude is delivered to China via oil pipelines such as the Eastern Siberia–Pacific Ocean (ESPO) route, which has become a particularly important component of China’s import portfolio. By early 2026, Russia has emerged as China’s top crude oil supplier, accounting for approximately 19.6% to over 20% of China’s total crude imports in 2024 and 2025. Imports frequently exceed 2 million barrels per day (bpd), driven by discounted prices on grades such as ESPO and Urals. These discounts are largely a consequence of Western sanctions imposed since 2022 in response to the Ukraine crisis, which have constrained Russia’s access to European markets as well as to Western shipping, insurance, and financial services.

This deepening energy interdependence is even more evident in the gas sector. The operational Power of Siberia pipeline—linking eastern Siberian gas fields to northeastern China—has rapidly scaled up deliveries to around 39 billion cubic meters (bcm) annually. Discussions are also underway to increase gas flows up to 44 bcm per year through upgrades and operational optimization.

The bilateral energy relationship is set to deepen further with the proposed Power of Siberia-2, designed to deliver up to 50 bcm of gas annually from western Siberia to China via Mongolia. However, this roughly 2,600-km pipeline remains closely tied to the broader pricing dynamics shaping Russia–China energy relations. Despite years of negotiations, progress has stalled primarily due to disagreements over gas pricing. China seeks to preserve discounted terms, while Moscow aims to secure higher returns to justify the investment. This impasse reflects a wider asymmetry in bargaining power. As Russia continues to offer gas at reduced prices amid limited alternative markets, Beijing faces little urgency to finalize a long-term agreement. Consequently, the future of the pipeline remains uncertain. This underscores the fact that infrastructure expansion is not merely a technical matter but also a function of shifting economic leverage between the two sides.

China’s Energy Bridge to Central Asia

Beyond the Russia–China axis, Central Asia plays a vital role in shaping Beijing’s overland energy architecture. However, similar patterns of constrained capacity and strategic recalibration can be observed across the region’s energy corridors. Region wide pipeline networks linking Kazakhstan and other Central Asian states to western China provide critical overland alternatives that bypass maritime chokepoints altogether. The Kazakhstan–China Oil Pipeline, operational since 2006, has a capacity of around 20 million tons per year (approximately 400,000 bpd) and typically delivers 250,000–400,000 bpd, accounting for roughly 3–5% of China’s total crude oil imports.

At the same time, the Russia–Ukraine war—particularly drone attacks on the Caspian Pipeline Consortium (CPC) facilities at Russia’s Black Sea port terminal at Novorossysk— has significantly disrupted Kazakhstan’s oil export infrastructure, prompting renewed efforts to diversify routes. During the second Caspian and Central Asia Oil Trading and Logistics Forum held in Baku on April 23, 2026, the Chairman of the Board of PetroCouncil.kz Assylbek Jakiyev highlighted the vulnerability of Kazakhstan’s existing export system, citing disruptions affecting routes linked to the CPC. He noted that Kazakhstan is actively evaluating two principal alternatives, the Trans-Caspian route via Azerbaijan (the Middle Corridor) and the China-bound export route supported by existing infrastructure. Although the China route offers immediate capacity of up to 20 million tons annually, its current utilization remains significantly below potential, at approximately 3 to 5 million tons, primarily due to operational constraints.

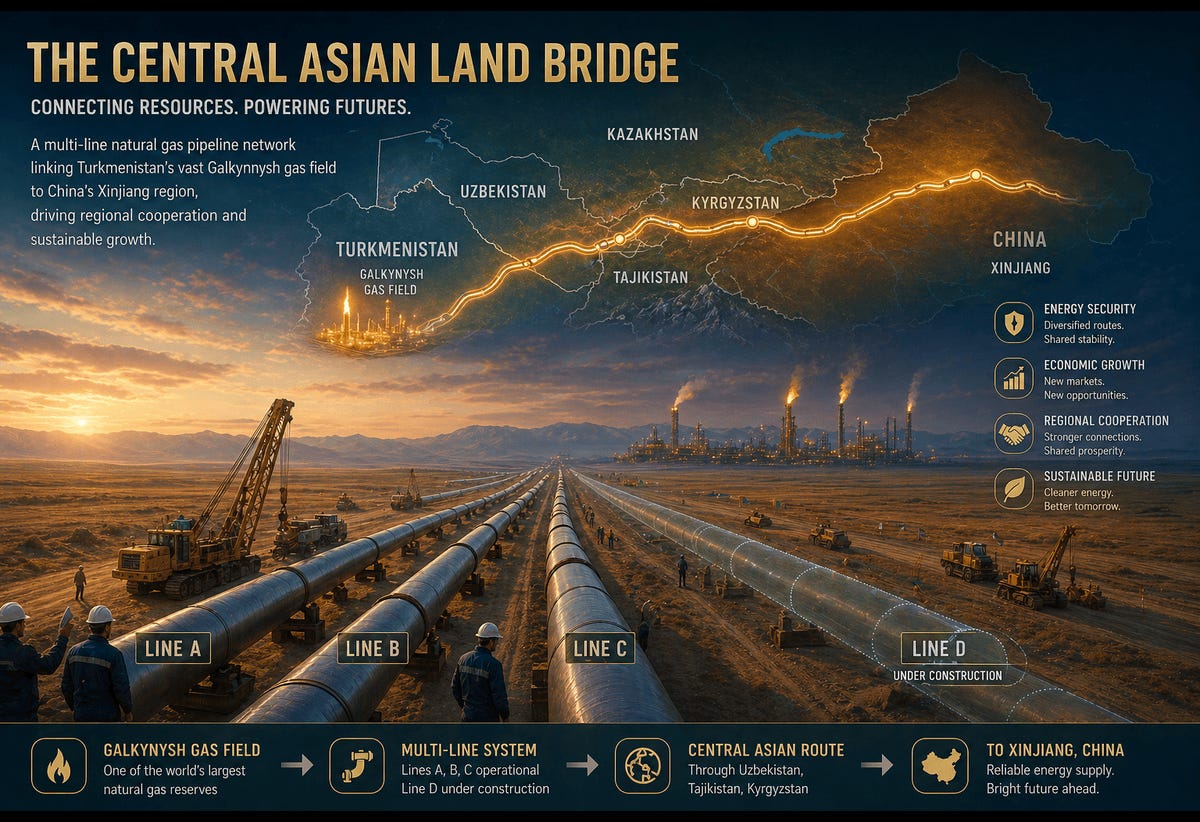

In parallel, the Central Asia–China Gas Pipeline—linking Turkmenistan, Uzbekistan, and Kazakhstan to China—supplies around 55 bcm of natural gas annually through its three existing lines (A, B, and C), with long-term agreements (particularly with Turkmenistan) targeting up to 65 bcm per year. This framework is expected to deepen further with the proposed Line D expansion, a fourth branch of the pipeline system designed to add 25–30 bcm per year via a new route through Uzbekistan, Tajikistan, and Kyrgyzstan. Although the project has faced delays since 2014 due to financing constraints and complex transit negotiations, it remains a strategically important priority for Beijing. Once the long-awaited Line D becomes operational, the Central Asia–China Gas Pipeline system will reach an annual capacity of approximately 85 billion cubic meters, making it the largest gas transmission system in Central Asia.

Importantly, this infrastructure expansion is reinforced by recent high-level political engagement between the two countries. During a meeting in Beijing on March 18, 2026, Xi Jinping and Turkmenistan’s National Leader and former president, Gurbanguly Berdimuhamedow held comprehensive talks aimed at deepening bilateral cooperation across multiple sectors, with energy remaining a central pillar. Both sides emphasized the importance of expanding cooperation in natural gas, with particular attention being paid to the continued development of the Galkynysh field and the strengthening of long-term supply arrangements. The meeting also highlighted efforts to align Turkmenistan’s development strategy with China’s Belt and Road Initiative, further embedding energy cooperation within a broader framework of connectivity and regional integration.

This momentum was further reinforced in subsequent engagements. During high-level talks held in Turkmenistan in mid-April 2026, Chinese Vice Premier Ding Xuexiang and Gurbanguly Berdimuhamedow reaffirmed their commitment to deepening bilateral energy cooperation, with natural gas remaining central to the partnership. The discussions— held alongside the launch of new development phases at the Galkynysh gas field—emphasized expanding the scale of gas cooperation and accelerating key joint projects. A central outcome was an agreement to further develop Turkmenistan’s vast gas reserves and strengthen long-term supply arrangements to China through existing and planned pipeline infrastructure.

Shortly thereafter, Türkmengaz signed a $4.6 billion gas field contract with China National Petroleum Corporation (CNPC) to design and construct production facilities capable of processing up to 10 bcm of gas annually as part of the development of Phase 4 of the Galkynyshgas field. As one of the world’s largest natural gas fields, Galkynysh forms the backbone of Turkmenistan’s export capacity to China via the Central Asia–China pipeline network.

Still, Central Asia provides a relatively modest share of China’s crude oil imports but remains a major source of pipeline gas, at times accounting for around one-third of the country’s natural gas imports. Beyond their quantitative contribution, these overland supply channels are strategically indispensable, enabling stable, long-term deliveries into China’s Xinjiang region under frameworks such as the Belt and Road Initiative. To some extent, they mitigate China’s exposure to vulnerable maritime chokepoints while reinforcing its broader energy diversification strategy.

Beyond its deepening engagement with Central Asia—especially the energy-rich Caspian littoral states of Kazakhstan and Turkmenistan—China is well positioned to expand its energy and connectivity footprint across the wider Caspian basin, where Azerbaijan is emerging as a pivotal energy and transit hub. Offshore production from the Azeri-Chirag-Gunashli (ACG) complex and the Shah Deniz gas field underpins Azerbaijan’s export capacity, while logistics centered on Baku—supported by the Port of Baku and its integration with the Port of Aktau in Kazakhstan and Turkmenbashi International Seaport in Turkmenistan—could facilitate the trans-Caspian movement of hydrocarbons, including potential eastward flows over the longer term.

China’s involvement in Azerbaijan’s hydrocarbon sector remains limited, particularly in core offshore oil and gas projects dominated by Western and regional consortia. Its presence is more visible in renewables, technical services, and infrastructure cooperation across various regions of Azerbaijan. By contrast, China is far more active along the eastern Caspian littoral, particularly on Kazakhstan’s shores. Through China National Petroleum Corporation (CNPC), Beijing controls about 86% of the Aktobe oil fields and holds roughly 8.4% in the Kashagan oil field. It is also more broadly engaged in pipeline and energy infrastructure, though it does not exercise dominant control over the sector as a whole.

Concurrently, Azerbaijan’s growing alignment with Central Asian producers—reinforced through multilateral frameworks such as the C6 platform and the Organization of Turkic States—is consolidating a more cohesive trans-Caspian corridor. This integration enhances multimodal flexibility and enables the rerouting of flows in response to geopolitical or market disruptions. Rising Asian demand—evidenced by Japan’s recent efforts to secure crude from Azerbaijan’s and Kazakhstan’s offshore oil fields—further underscores the system’s growing multidirectional character. For Beijing, deeper engagement with this Azerbaijan-centered network is unlikely to generate immediate large-scale import volumes, given existing infrastructural and capacity constraints. However, this would reinforce a parallel, non-Russian Eurasian corridor, diversifying supply pathways and reducing concentration risk, while enhancing China’s long-term strategic optionality within an increasingly complex and interdependent energy landscape.

Outlook

Despite significant progress in diversifying supply routes and expanding overland energy corridors, China’s energy security strategy remains fundamentally constrained by structural realities. The country continues to rely heavily on Gulf hydrocarbons—particularly oil—much of which still transits through the Strait of Hormuz. In practice, no combination of pipelines from Russia or Central Asia can fully replicate the scale, flexibility, and liquidity of global seaborne energy markets. Crucially, pipeline-based supply remains limited in scale relative to the vast volumes transported via maritime routes, underscoring the structural limits of overland diversification.

At the same time, China’s pivot toward continental suppliers introduces a new set of risks rather than eliminating existing ones. Deepening dependence on Russia raises the prospect of strategic overexposure to a single supplier operating under sanctions, potentially enhancing Moscow’s leverage over pricing and long-term contractual arrangements. Meanwhile, Central Asian energy corridors remain constrained by limited capacity, complex transit frameworks, and infrastructure vulnerabilities. Key interregional energy initiatives, such as the Power of Siberia 2 pipeline and Central Asia–China Gas Pipeline Line D, continue to face delays, uncertainty, and political friction, underscoring the fragility of China’s long-term diversification strategy.

To this end, the Hormuz disruption reveals a central contradiction in China’s energy strategy. While Beijing has managed to reduce some of its most acute vulnerabilities, it remains deeply reliant on global transport networks, underscoring the persistent limits of its diversification efforts. Over the longer term, China’s push toward renewable energy and electrification may further mitigate its exposure to external shocks. What emerges is not a fully secure system, but a more complex and layered one—where resilience has improved, yet systemic risk remains deeply embedded.

About the Author:

Vusal Guliyev is a frequent contributor to The Saratoga Foundation. He is a Sinologist, TCSOL Specialist, and Policy Analyst specializing in the geopolitical affairs of Eurasia and the Indo-Pacific region. Mr. Guliyev currently works as a Leading Advisor at the Baku-based Center of Analysis of International Relations (AIR Center) and serves as the Head of the Shanghai Office at AZEGLOB Consulting Group.

Thank you for your support! Please remember that The Saratoga Foundation is a non-profit 501(c)(3) organization. Your donations are fully tax-deductible. If you seek to support The Saratoga Foundation, you can make a one-time donation by clicking on the PayPal link below! You can also subscribe to our website to support our work.

https://www.paypal.com/donate/?hosted_button_id=XFCZDX6YVTVKA